Check out the latest research papers SwapsInfo First Quarter of 2025.

The CFTC’s updated post-initial minimum block and cap sizes, effective October 7, 2024, have resulted in higher year-over-year disclosed traded notional for IRD and index credit derivatives.

OIS and fixed-for-floating transactions are now grouped into three tenor-based buckets: up to and including one year, over one year up to and including five years, and over five years. This categorization provides a more detailed and transparent view of swaps trading activity across distinct tenor segments.

ISDA has expanded its SwapsInfo derivatives database and website to include European credit default swaps (CDS) trading activity, creating a more comprehensive picture of derivatives trading in the EU, UK and US.

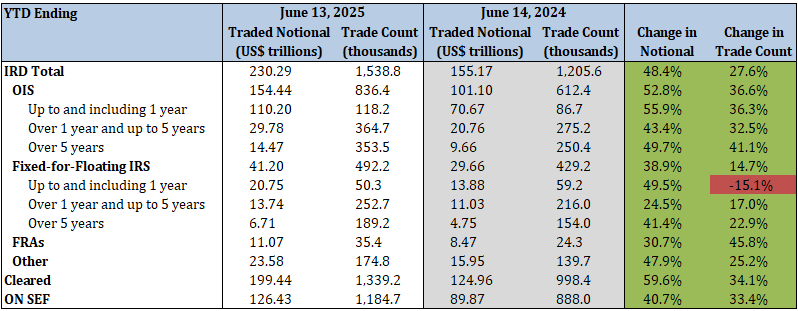

Interest Rate Derivatives

2025 YTD vs. 2024 YTD

- Total IRD traded notional and trade count increased by 48.4% and 27.6%, respectively

- YTD 2025, 71.4% of OIS traded notional had tenors up to and including one year, 19.3% between one and five years, and 9.4% over five years

- YTD 2025, 50.4% of fixed-for-floating IRS traded notional had tenors up to and including one year, 33.3% between one and five years, and 16.3% over five years

- 86.6% of total traded notional was cleared vs. 80.5% last year

- 54.9% of total traded notional was executed on SEFs vs. 57.9% last year

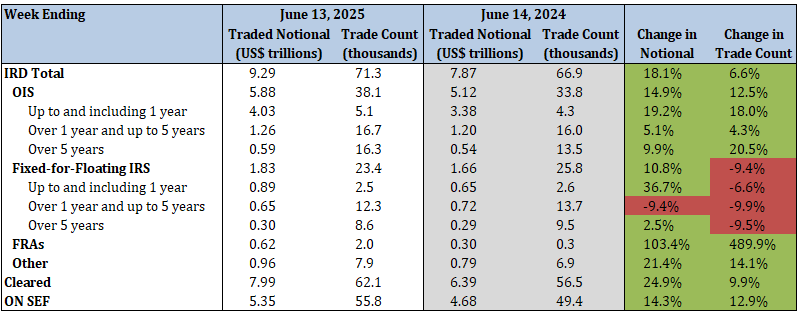

2025 Current Week vs. 2024 Current Week

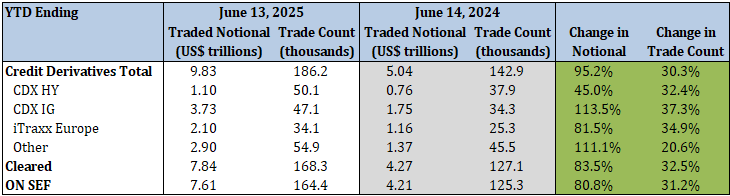

Credit Derivatives Reported under CFTC Regulations

2025 YTD vs. 2024 YTD

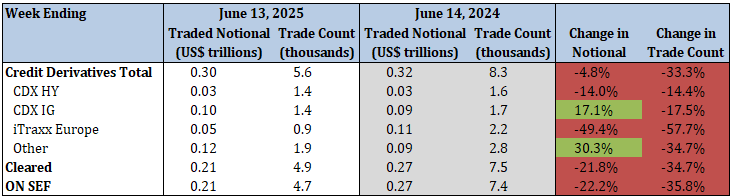

- Total index credit derivatives traded notional and trade count increased by 95.2% and 30.3%, respectively

- CDX HY traded notional and trade count increased by 45.0% and 32.4%, respectively

- CDX IG traded notional and trade count increased by 113.5% and 37.3%, respectively

- iTraxx Europe traded notional and trade count increased by 81.5% and 34.9%, respectively

- 79.7% of total traded notional was cleared vs. 84.8% last year

- 77.4% of total traded notional was executed on SEFs vs. 83.6% last year

2025 Current Week vs. 2024 Current Week

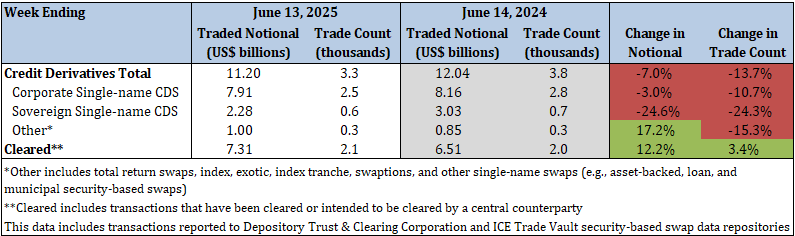

Credit Derivatives Reported under SEC Regulations

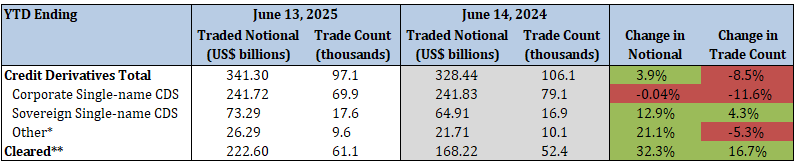

2025 YTD vs. 2024 YTD

- Total security-based credit derivatives traded notional increased by 3.9%, while trade count decreased by 8.5%

- Corporate single-name CDS traded notional was largely unchanged, while trade count decreased by 11.6%

- Sovereign single-name CDS traded notional and trade count increased by 12.9% and 4.3%, respectively

- 65.2% of total traded notional was cleared vs. 51.2% last year

2025 Current Week vs. 2024 Current Week