ISDA has expanded its SwapsInfo website to include interest rate derivatives trading activity reported in the EU and UK. The new data is based on transactions publicly reported by 30 European approved publication arrangements and trading venues.

Check out the latest Transition to RFRs Review: First Quarter of 2022.

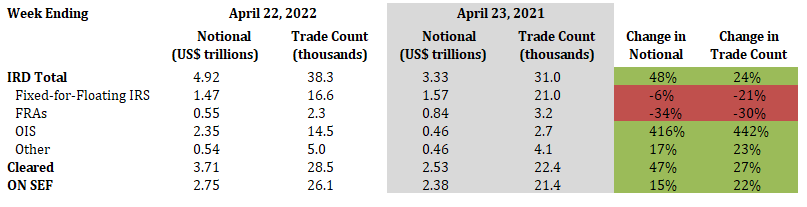

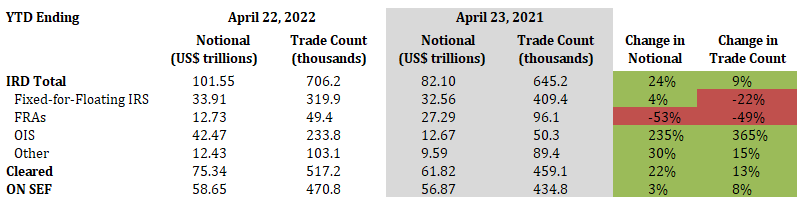

Interest Rate Derivatives

2022 Current Week vs. 2021 Current Week

- Total IRD traded notional and trade count increased by 48% and 24%, respectively

- Fixed-for-floating IRS traded notional and trade count decreased by 6% and 21%, respectively

- FRAs traded notional and trade count decreased by 34% and 30%, respectively

- OIS traded notional and trade count increased by 416% and 442%, respectively

- 76% of total traded notional was cleared, flat compared with last year

- 56% of total traded notional was executed on SEFs vs. 72% last year

2022 YTD vs. 2021 YTD

- Total IRD traded notional and trade count increased by 24% and 9%, respectively

- Fixed-for-floating IRS traded notional increased by 4%, while trade count decreased by 22%

- FRAs traded notional and trade count decreased by 53% and 49%, respectively

- OIS traded notional and trade count increased by 235% and 365%, respectively

- 74% of total traded notional was cleared vs. 75% last year

- 58% of total traded notional was executed on SEFs vs. 69% last year

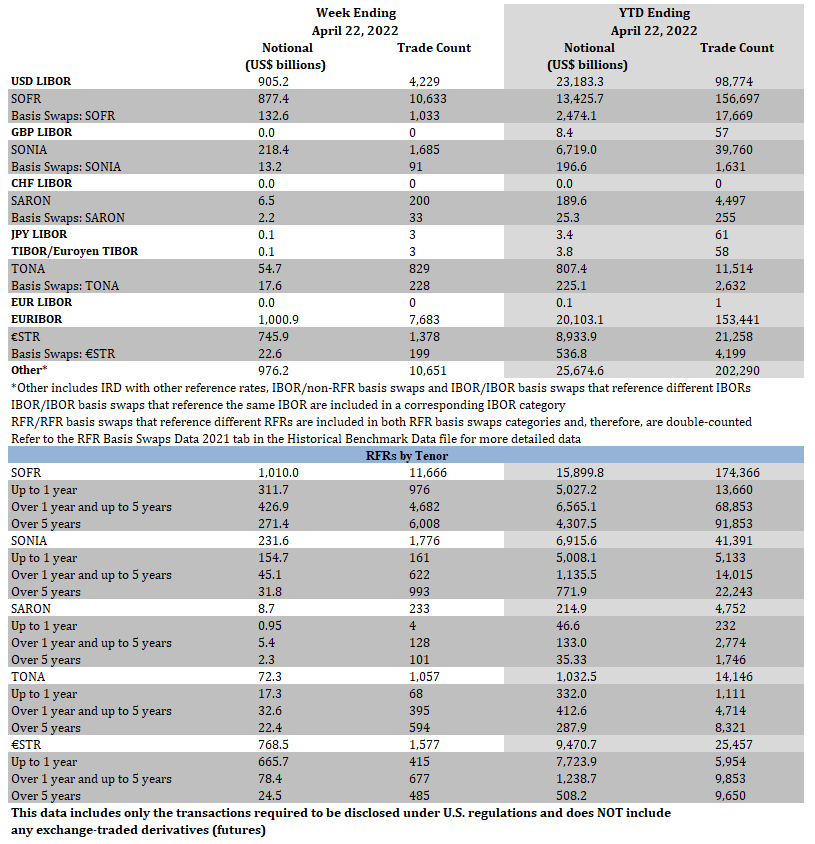

Interest Rate Derivatives: Benchmark Data

Week Ending April 22, 2022

- SOFR traded notional totaled $1.0 trillion, including $132.6 billion of basis swaps. Trade count totaled 11.7 thousand, including 1.0 thousand basis swaps

- SONIA traded notional totaled $231.6 billion, including $13.2 billion of basis swaps. Trade count totaled 1.8 thousand, including 91 basis swaps

- SARON traded notional totaled $8.7 billion, including $2.2 billion of basis swaps. Trade count totaled 233, including 33 basis swaps

- TONA traded notional totaled $72.3 billion, including $17.6 billion of basis swaps. Trade count totaled 1.1 thousand, including 228 basis swaps

- €STR traded notional totaled $768.5 billion, including $22.6 billion of basis swaps. Trade count totaled 1.6 thousand, including 199 basis swaps

YTD Ending April 22, 2022

- SOFR traded notional totaled $15.9 trillion, including $2.5 trillion of basis swaps. Trade count totaled 174.4 thousand, including 17.7 thousand basis swaps

- SONIA traded notional totaled $6.9 trillion, including $196.6 billion of basis swaps. Trade count totaled 41.4 thousand, including 1.6 thousand basis swaps

- SARON traded notional totaled $214.9 billion, including $25.3 billion of basis swaps. Trade count totaled 4.8 thousand, including 255 basis swaps

- TONA traded notional totaled $1.0 trillion, including $225.1 billion of basis swaps. Trade count totaled 14.2 thousand, including 2.6 thousand basis swaps

- €STR traded notional totaled $9.5 trillion, including $536.8 billion of basis swaps. Trade count totaled 25.5 thousand, including 4.2 thousand basis swaps

Click Here to View Historical Benchmark Data

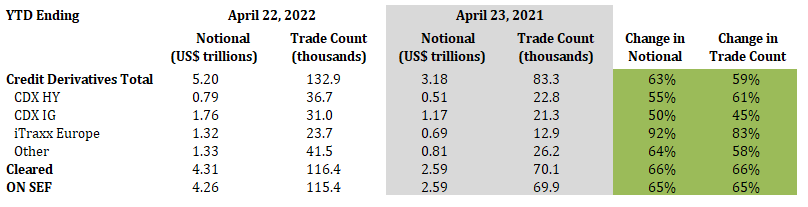

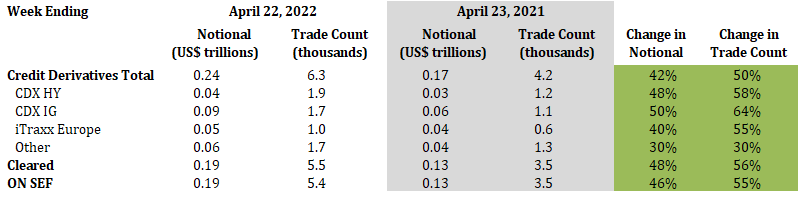

Credit Derivatives

2022 Current Week vs. 2021 Current Week

- Total credit derivatives traded notional and trade count increased by 42% and 50%, respectively

- CDX HY traded notional and trade count increased by 48% and 58%, respectively

- CDX IG traded notional and trade count increased by 50% and 64%, respectively

- iTraxx Europe traded notional and trade count increased by 40% and 55%, respectively

- 80% of total traded notional was cleared vs. 77% last year

- 79% of total traded notional was executed on SEFs vs. 77% last year

2022 YTD vs. 2021 YTD

- Total credit derivatives traded notional and trade count increased by 63% and 59%, respectively

- CDX HY traded notional and trade count increased by 55% and 61%, respectively

- CDX IG traded notional and trade count increased by 50% and 45%, respectively

- iTraxx Europe traded notional and trade count increased by 92% and 83%, respectively

- 83% of total traded notional was cleared vs. 82% last year

- 82% of total traded notional was executed on SEFs vs. 81% last year