Dear Readers,

Starting this September, we are tracking trade volumes for major IBORs and risk-free rates (RFRs), including SOFR, SONIA, SARON and TONA. Please see benchmark data below. This data covers only trades reported to DTCC and Bloomberg SDRs, which are required to be disclosed under US regulatory guidelines.

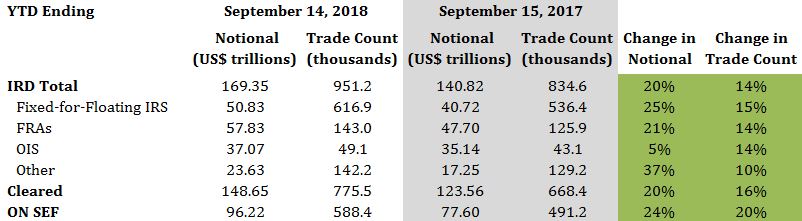

Interest Rate Derivatives

2018 YTD vs. 2017 YTD

- Total IRD traded notional and trade count increased by 20% and 14%, respectively

- Fixed-for-floating IRS traded notional and trade count increased by 25% and 15%, respectively

- FRAs traded notional and trade count increased by 21% and 14%, respectively

- OIS traded notional and trade count increased by 5% and 14%, respectively

- 88% of total traded notional was cleared, flat compared with last year

- 57% of total traded notional was executed On SEF vs. 55% last year

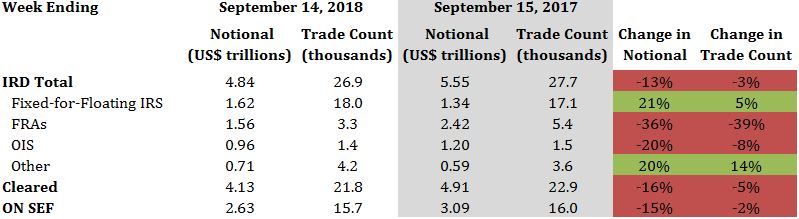

2018 Current Week vs. 2017 Current Week

- Total IRD traded notional and trade count decreased by 13% and 3%, respectively

- Fixed-for-floating IRS traded notional and trade count increased by 21% and 5%, respectively

- FRAs traded notional and trade count decreased by 36% and 39%, respectively

- OIS traded notional and trade count decreased by 20% and 8%, respectively

- 85% of total traded notional was cleared vs. 89% last year

- 54% of total traded notional was executed On SEF vs. 56% last year

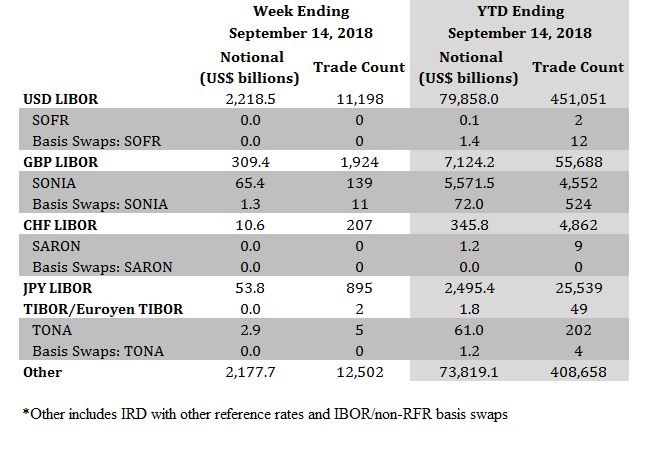

Interest Rate Derivatives: Benchmark Data

Week Ending September 14, 2018

- SONIA traded notional totaled $66.7 billion, including $1.3 billion of basis swaps. Trade count totaled 150, including 11 basis swaps

- TONA traded notional and trade count was $2.9 billion and 5, respectively

- There were no SOFR and SARON trades

YTD Ending September 14, 2018

- SOFR traded notional totaled $1.5 billion, including $1.4 billion of basis swaps. Trade count totaled 14, including 12 basis swaps

- SONIA traded notional was $5.6 trillion, including $72.0 billion of basis swaps. Trade count totaled 5,076, including 524 basis swaps

- SARON traded notional and trade count was $1.2 billion and 9, respectively

- TONA traded notional totaled $62.2 billion, including $1.2 billion of basis swaps. Trade count totaled 206, including 4 basis swaps

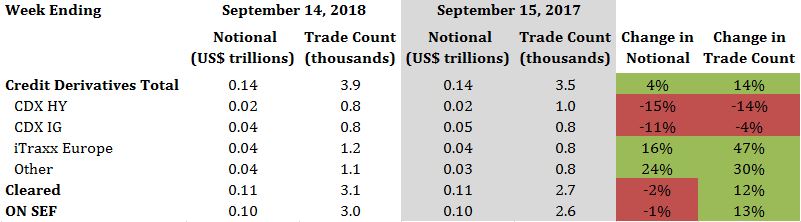

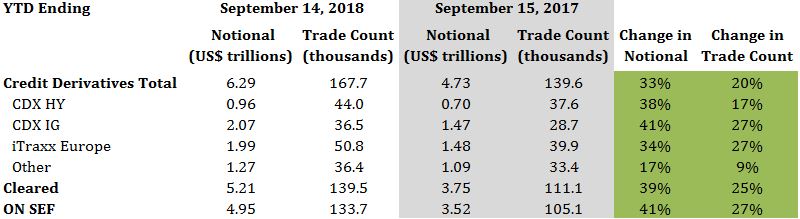

Credit Derivatives

2018 YTD vs. 2017 YTD

- Total credit derivatives traded notional and trade count increased by 33% and 20%, respectively

- CDX HY traded notional and trade count increased by 38% and 17%, respectively

- CDX IG traded notional and trade count increased by 41% and 27%, respectively

- iTraxx Europe traded notional and trade count increased by 34% and 27%, respectively

- 83% of total traded notional was cleared vs. 79% last year

- 79% of total traded notional was executed On SEF vs. 74% last year

2018 Current Week vs. 2017 Current Week

- Total credit derivatives traded notional and trade count increased by 4% and 14%, respectively

- CDX HY traded notional and trade count decreased by 15% and 14%, respectively

- CDX IG traded notional and trade count decreased by 11% and 4%, respectively

- iTraxx Europe traded notional and trade count increased by 16% and 47%, respectively

- 76% of total traded notional was cleared vs. 81% last year

- 73% of total traded notional was executed On SEF vs. 77% last year