Interest Rate Derivatives

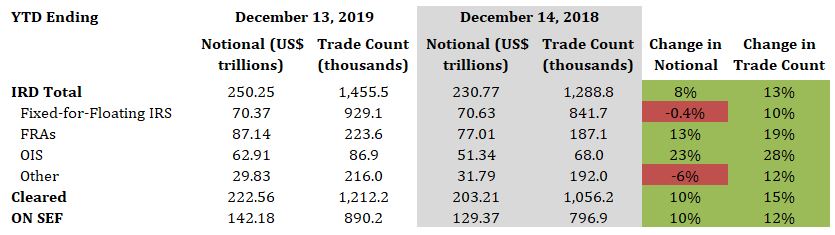

2019 YTD vs. 2018 YTD

- Total IRD traded notional and trade count increased by 8% and 13%, respectively

- Fixed-for-floating IRS traded notional decreased by 0.4%, while trade count increased by 10%

- FRAs traded notional and trade count increased by 13% and 19%, respectively

- OIS traded notional and trade count increased by 23% and 28%, respectively

- 89% of total traded notional was cleared vs. 88% last year

- 57% of total traded notional was executed On SEF vs. 56% last year

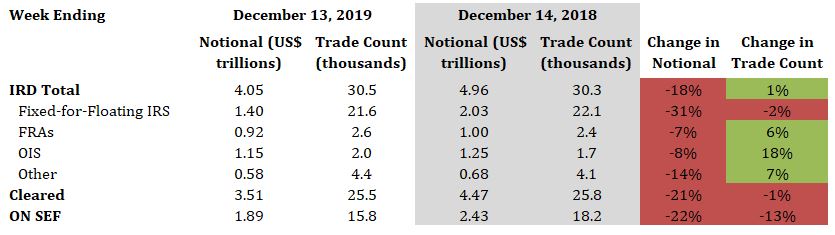

2019 Current Week vs. 2018 Current Week

- Total IRD traded notional decreased by 18%, while trade count increased by 1%

- Fixed-for-floating IRS traded notional and trade count decreased by 31% and 2%, respectively

- FRAs traded notional decreased by 7%, while trade count increased by 6%

- OIS traded notional decreased by 8%, while trade count increased by 18%

- 87% of total traded notional was cleared vs. 90% last year

- 47% of total traded notional was executed On SEF vs. 49% last year

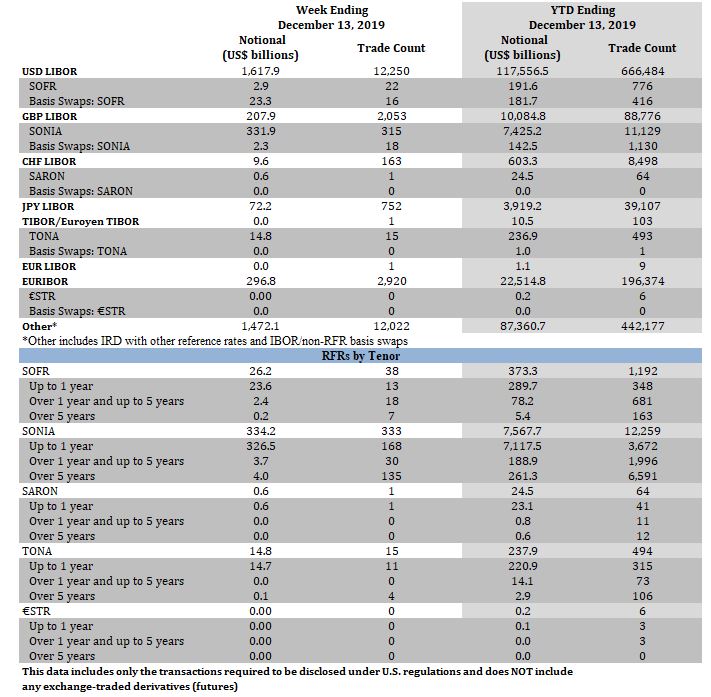

Interest Rate Derivatives: Benchmark Data

Week Ending December 13, 2019

- SOFR traded notional totaled $26.2 billion, including $23.3 billion of basis swaps. Trade count totaled 38, including 16 basis swaps

- SONIA traded notional totaled $334.2 billion, including $2.3 billion of basis swaps. Trade count totaled 333, including 18 basis swaps

- SARON traded notional and trade count was $600 million and 1, respectively

- TONA traded notional and trade count was $14.8 billion and 15, respectively

- There were no €STR trades

YTD Ending December 13, 2019

- SOFR traded notional totaled $373.3 billion, including $181.7 billion of basis swaps. Trade count totaled 1,192 including 416 basis swaps

- SONIA traded notional totaled $7.6 trillion, including $142.5 billion of basis swaps. Trade count totaled 12,259, including 1,130 basis swaps

- SARON traded notional and trade count was $24.5 billion and 64, respectively

- TONA traded notional totaled $237.9 billion, including $1.0 billion of basis swaps. Trade count totaled 494, including 1 basis swap

- €STR traded notional and trade count was $200 million and 6, respectively

Click Here to View Historical Benchmark Data

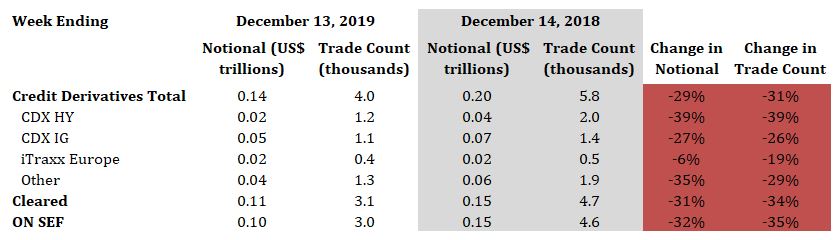

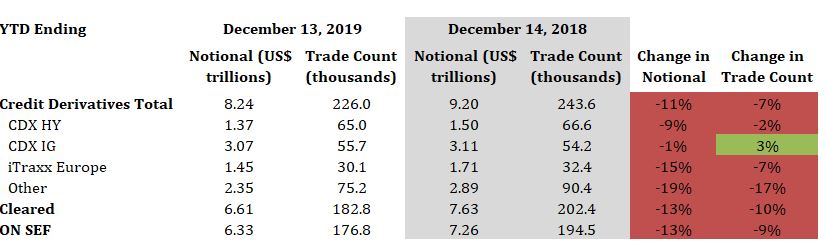

Credit Derivatives

2019 YTD vs. 2018 YTD

- Total credit derivatives traded notional and trade count decreased by 11% and 7%, respectively

- CDX HY traded notional and trade count decreased by 9% and 2%, respectively

- CDX IG traded notional decreased by 1%, while trade count increased by 3%

- iTraxx Europe traded notional and trade count decreased by 15% and 7%, respectively

- 80% of total traded notional was cleared vs. 83% last year

- 77% of total traded notional was executed On SEF vs. 79% last year

2019 Current Week vs. 2018 Current Week

- Total credit derivatives traded notional and trade count decreased by 29% and 31%, respectively

- CDX HY traded notional and trade count both decreased by 39%

- CDX IG traded notional and trade count decreased by 27% and 26%, respectively

- iTraxx Europe traded notional and trade count decreased by 6% and 19%, respectively

- 76% of total traded notional was cleared vs. 78% last year

- 72% of total traded notional was executed On SEF vs.75% last year