Due to a change in reporting logic within the DTCC SDR on November 21st, 2020, the clearing status was not consistently reported by some participants. Therefore, clearing metrics are not included in the below analysis.

Data from ISDA SwapsInfo for the week ending January 1, 2021. Annual metrics for 2020 will be published in the SwapsInfo Full Year 2020 and Transition to RFRs Review Full Year 2020 reports later in January.

Interest Rate Derivatives

2021 Current Week vs. 2020 Current Week

- Total IRD traded notional and trade count decreased by 77% and 45%, respectively

- Fixed-for-floating IRS traded notional and trade count decreased by 40% and 36%, respectively

- FRAs traded notional and trade count decreased by 97% and 99%, respectively

- OIS traded notional and trade count decreased by 73% and 55%, respectively

- 45% of total traded notional was executed On SEF vs. 66% last year

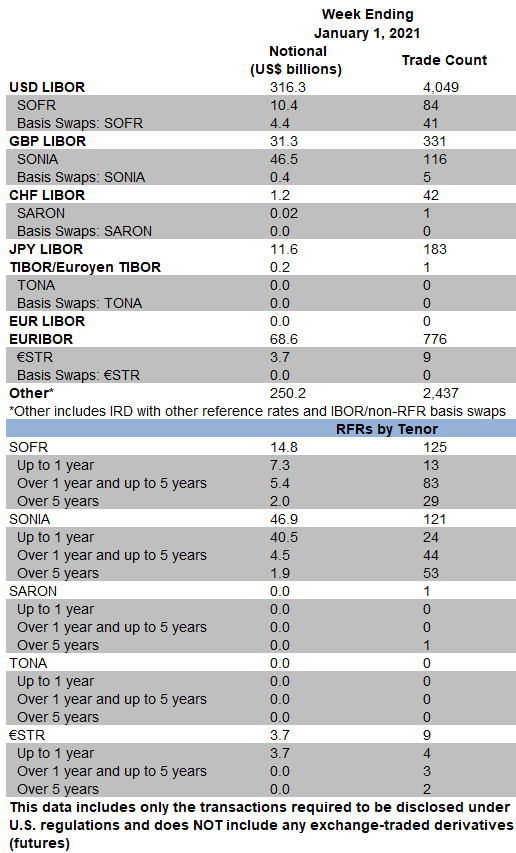

Interest Rate Derivatives: Benchmark Data

Week Ending January 1, 2021

- SOFR traded notional totaled $14.8 billion, including $4.4 billion of basis swaps. Trade count totaled 125, including 41 basis swaps

- SONIA traded notional totaled $46.9 billion, including $0.4 billion of basis swaps. Trade count totaled 121, including 5 basis swaps

- SARON traded notional and trade count was $20 million and 1, respectively

- There were no TONA trades

- €STR traded notional and trade count was $3.7 billion and 9, respectively

Click Here to View Historical Benchmark Data

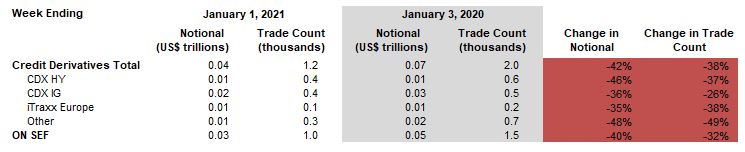

Credit Derivatives

2021 Current Week vs. 2020 Current Week

- Total credit derivatives traded notional and trade count decreased by 42% and 38%, respectively

- CDX HY traded notional and trade count decreased by 46% and 37%, respectively

- CDX IG traded notional and trade count decreased by 36% and 26%, respectively

- iTraxx Europe traded notional and trade count decreased by 35% and 38%, respectively

- 76% of total traded notional was executed On SEF vs. 74% last year