Due to a change in reporting logic within the DTCC SDR on November 21st, 2020, the clearing status was not consistently reported by some participants. Therefore, clearing metrics are not included in the below analysis.

ISDA-Clarus RFR Adoption Indicator declined to 8.3% in November compared to 11.6% the prior month. The indicator tracks how much global trading activity (as measured by DV01) is conducted in cleared over-the-counter and exchange-traded interest rate derivatives that reference the identified risk-free rates (RFRs) in six major currencies. The latest November report is available here.

Interest Rate Derivatives

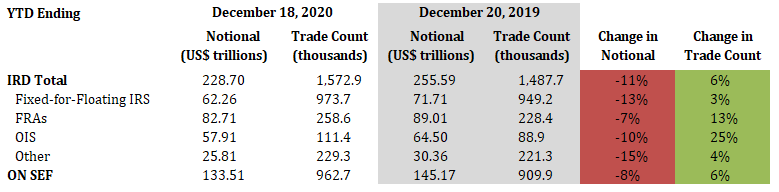

2020 YTD vs. 2019 YTD

- Total IRD traded notional decreased by 11%, while trade count increased by 6%

- Fixed-for-floating IRS traded notional decreased by 13%, while trade count increased by 3%

- FRAs traded notional decreased by 7%, while trade count increased by 13%

- OIS traded notional decreased by 10%, while trade count increased by 25%

- 58% of total traded notional was executed On SEF vs. 57% last year

2020 Current Week vs. 2019 Current Week

- Total IRD traded notional decreased by 17%, while trade count increased by 1%

- Fixed-for-floating IRS traded notional and trade count decreased by 9% and 0.01%, respectively

- FRAs traded notional decreased by 2%, while trade count increased by 40%

- OIS traded notional decreased by 34%, while trade count increased by 24%

- 54% of total traded notional was executed On SEF vs. 46% last year

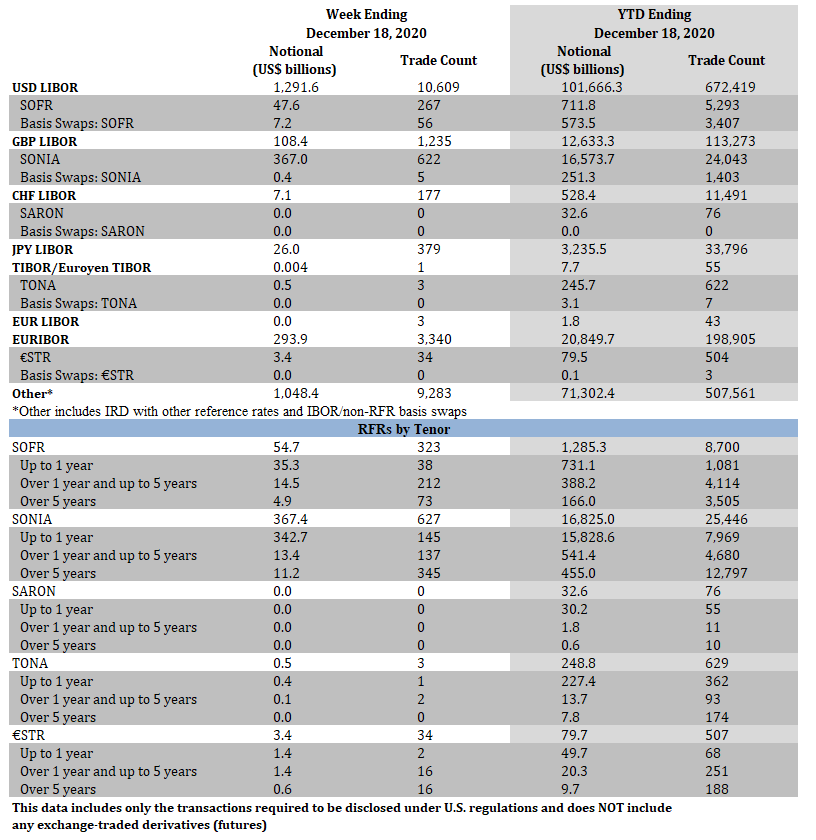

Interest Rate Derivatives: Benchmark Data

Week Ending December 18, 2020

- SOFR traded notional totaled $54.7 billion, including $7.2 billion of basis swaps. Trade count totaled 323, including 56 basis swaps

- SONIA traded notional totaled $367.4 billion, including $0.4 billion of basis swaps. Trade count totaled 627, including 5 basis swaps

- There were no SARON trades

- TONA traded notional and trade count was $0.5 billion and 3, respectively

- €STR traded notional and trade count was $3.4 billion and 34, respectively

YTD Ending December 18, 2020

- SOFR traded notional totaled $1.3 trillion, including $573.5 billion of basis swaps. Trade count totaled 8,700, including 3,407 basis swaps

- SONIA traded notional totaled $16.8 trillion, including $251.3 billion of basis swaps. Trade count totaled 25,446, including 1,403 basis swaps

- SARON traded notional and trade count was $32.6 billion and 76, respectively

- TONA traded notional totaled $248.8 billion, including $3.1 billion of basis swaps. Trade count totaled 629, including 7 basis swaps

- €STR traded notional totaled $79.7 billion, including $0.1 billion of basis swaps. Trade count totaled 507, including 3 basis swaps

Click Here to View Historical Benchmark Data

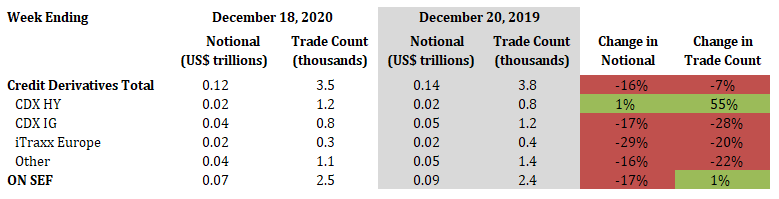

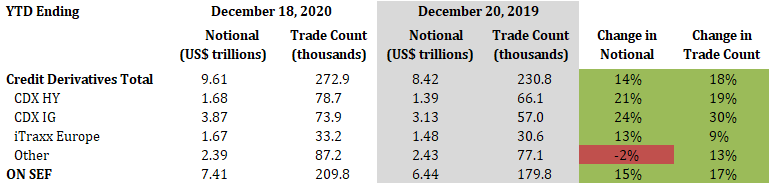

Credit Derivatives

2020 YTD vs. 2019 YTD

- Total credit derivatives traded notional and trade count increased by 14% and 18%, respectively

- CDX HY traded notional and trade count increased by 21% and 19%, respectively

- CDX IG traded notional and trade count increased by 24% and 30%, respectively

- iTraxx Europe traded notional and trade count increased by 13% and 9%, respectively

- 77% of total traded notional was executed On SEF vs. 76% last year

2020 Current Week vs. 2019 Current Week

- Total credit derivatives traded notional and trade count decreased by 16% and 7%, respectively

- CDX HY traded notional and trade count increased by 1% and 55%, respectively

- CDX IG traded notional and trade count decreased by 17% and 28%, respectively

- iTraxx Europe traded notional and trade count decreased by 29% and 20%, respectively

- 65% of total traded notional was executed On SEF vs. 66% last year